No doubt if you’ve been inside of any of the major investment firms like Fidelity, Vanguard, Black Rock, etc. you’ll hear Mobb Deep’s 1995 Survival of Fittest on constant repeat if you listen closely enough. It fits because the words “there’s a war goin’ on outside no man is safe from” has never rung truer, at least when it comes to fees and mutual funds.

In the War on Fees, Schwab is the latest entrant and they’ve shown up to the party with their big guns. Schwab has cut their fees on their S&P 500 Index Fund (SWPPX), Total Stock Fund (SWTSX), Small-Cap Index Fund (SWSSX), International Index Fund(SWISX), US Aggregate Bond Fund (SWAGX) and more. Take a peek at Schwab verse the powerhouses of Vanguard and Fidelity:

https://www.schwab.com/public/schwab/nn/m/indexfunds.html

These lower fees are great for the investing public, it rightfully takes money out of deep coffers of Wall Street firms and places it back into the piggy banks of individual investors. The rapid trend in declining fees just proves these costs were nothing but a fat profit center for investment firms all along. These inflated expenses were an easy money grab, collecting a few extra monthly dollars from consumers to the tune of hundreds of millions of dollars a year in profit.

Fees Explained

Fees are listed as an ‘expense ratio.’ This is an annual fee to cover expenses like management, administration, operating costs, etc. You can roughly calculate the annual cost by multiplying the expense ratio by the total assets in your fund (this calculation gets more complex when you have to account for monthly contributions like to a 401k). Below is a hypothetical example between Schwab and Vanguard of the potential costs over a 10 year period of an initial $10k investment in a S&P 500 Index Fund:

In the above you have a $175 difference over 10 years which may not seem that much to you. However what if you had $100K in that fund? You would surely have some strong emotions about losing out on $1,750. Expand the same analysis over 20 years for $100K and your loss balloons to $6,300 (over three times as much due to compounding)! That’s enough to make anyone sick to their stomach. To make matters worse the investment firm gets their fees rain or sun, they make money whether your fund’s value goes up or down.

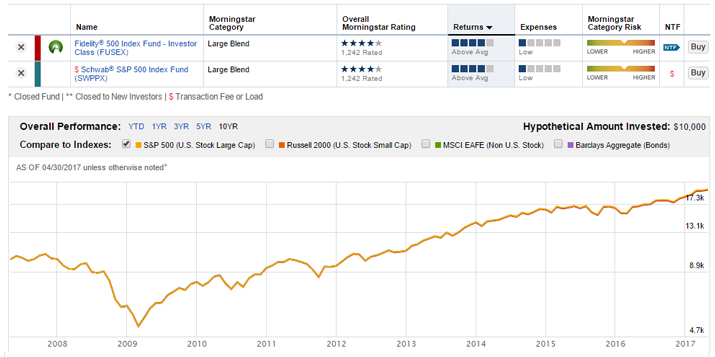

Fund Performance

Although fees are an important part, performance rules over everything. There is no glory in owning a under-performing low-cost mutual fund. So the million dollar question is how do these Schwab funds measure up against their competitors? Let compare Schwab’s S&P 500 Index Fund (SWPPX) vs. Fidelity’s FUSEX and the S&P 500 Index:

As you can see above it’s all virtually the same, the lines for the S&P 500, Fidelity and Schwab are all indistinguishable. Next let’s test the Schwab’s Total Stock Market Index Fund (SWTSX) vs. Vanguard’s VTSMX:

Another test and another A+ passing grade. The performance between the two funds is nearly identical over the long term. Last, let’s test small cap stocks: Schwab’s SWSSX vs. Fidelity’s FSSPX:

Once again the results are the same, the two funds are nearly identical. Schwab appears to have done its part in ratcheting up the stakes in the War on Fees. Their index funds (at least the ones tested above) have approx. the same performance and lower costs relative to the major players in the industry. If you have index funds in your portfolio I would definitely research the expense ratios vs. what Schwab is offering, especially if you are starting out with less than $10k.

You see in the earlier table the expense ratios are lower for investors with over $10k in an index fund with Fidelity or Vanguard. In this scenario the difference in fees vs. Schwab is less stark, only 0.01%. For $100k invested over 20 years assuming a 7.5% annual return this equates to only about $160. If you have other products with Fidelity or Vanguard you may prefer to keep everything in one place for easier management, 0.01% isn’t really much of an incentive to go through the trouble of making a switch.

Schwab has lowered fees on their ETFs too and even more mutual funds than mentioned in the post. If you have any index funds in your portfolio it may be worth while to do the research to see if Schwab has a product that can give you the same performance at a lower cost.